The omnibus proposals recently published by the EU Commission, which aim at amending the EU’s Corporate Sustainability Reporting Directive (CSRD), confirmed that most non-listed small and medium-sized enterprises (SMEs) will likely remain exempt from mandatory sustainability reporting. This regulatory clarification makes voluntary frameworks such as the Voluntary Sustainability Reporting Standard for non-listed SME (VSME), published in draft form by EFRAG in December 2024, all the more relevant. This standard was designed specifically for SMEs that are not publicly listed, offering a simplified and voluntary approach to sustainability reporting. Their development responds to the growing demand for consistent and comparable ESG data from SMEs, driven by supply chain expectations, financing conditions, and evolving market requirements.

However, as the draft VSME was published before the omnibus proposals, which exempt many SMEs – including listed ones – from reporting requirements, the VSME will receive more attention. In particular, companies that have prepared for CSRD reporting, will no longer be in scope of the CSRD and now have a functioning ESG reporting, strategy and governance process in place will be looking for a reliable and recognised framework as an alternative to the ESRS.

Given this increased focus, we expect to see changes to the draft before it becomes effective in order reflect the new target group of the VSME. Many market participants are indeed expecting or hoping for the inclusion of a double materiality assessment (DMA) to be included in the VSME.

The VSME Standard – why does it matter?

Small and medium-sized enterprises (SMEs) are the cornerstone of the European economy, accounting for 99% of all businesses and a significant share of employment and innovation. However, most SMEs are not currently or, due to the EU Commissions Omnibus proposal, will not be subject to mandatory sustainability reporting under the EU’s Corporate Sustainability Reporting Directive (CSRD).

Nevertheless, SMEs increasingly face pressure from banks, investors, and corporate clients to disclose ESG-related information. The VSME Standard offer a streamlined and proportionate framework that can help SMEs address these information demands without being overburdened by complexity.

What is included in the VSME Standard?

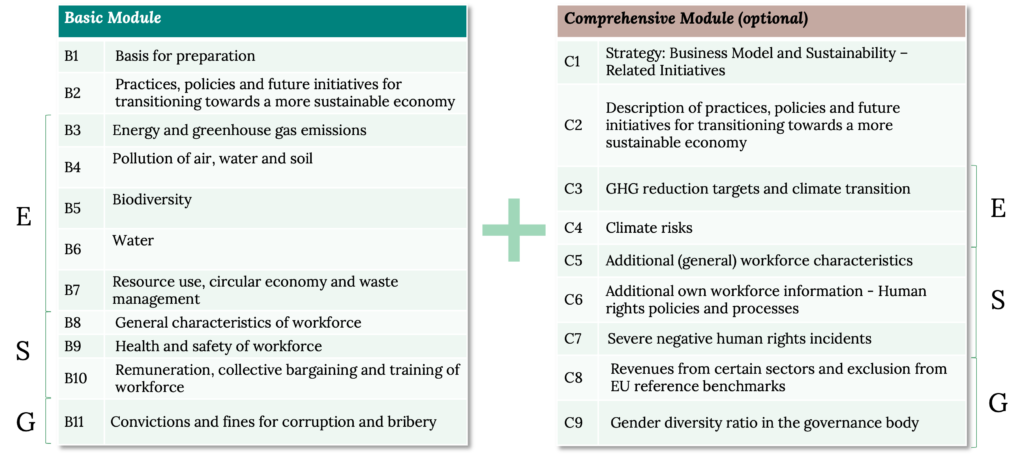

The December 2024 draft of the VSME Sustainability Reporting Standard introduces a modular framework consisting of two reporting options:

Basic Module

This simplified module allows SMEs to report on essential sustainability information.

It is designed to minimise reporting burdens while covering key environmental, social, and governance topics.

The information is primarily qualitative, easy to understand, and aimed at satisfying the needs of most stakeholders, particularly in value chains.

Comprehensive Module

This module is intended for SMEs with more advanced sustainability practices or those facing higher demands from external stakeholders.

It includes additional quantitative and policy-related disclosures.

While still voluntary and simplified in comparison, the comprehensive module brings SMEs closer in line with the CSRD requirements, helping them prepare for potential future regulatory obligations.

Both modules are intended to be flexible and scalable, allowing SMEs to begin with the Basic Module and expand their reporting scope over time. Note that the current version of the VSME does not include a materiality assessment.

Key Benefits for SMEs

- Respond to stakeholder expectations: VSME reporting helps SMEs respond to ESG information requests from clients, investors, and lenders.

- Streamlined reporting: By using a standardised format, SMEs can reduce the administrative burden of responding to multiple individual ESG questionnaires.

- Future-proofing: As sustainability regulations expand, early adoption of the VSME Standard helps SMEs prepare and build internal capacity.

- Improve access to finance: Transparent ESG data can improve creditworthiness and align SMEs with sustainability-linked financing instruments.

Challenges to consider

- Capacity constraints: Many SMEs lack dedicated sustainability staff or expertise, making even simplified reporting a challenge.

- Data availability: Gathering reliable sustainability data can be challenging, especially for smaller businesses without existing systems and processes for recording, managing and analysing sustainability data.

- Adoption incentives: As the standard is voluntary, uptake may depend heavily on recognition and encouragement by financial institutions and supply chain leaders.

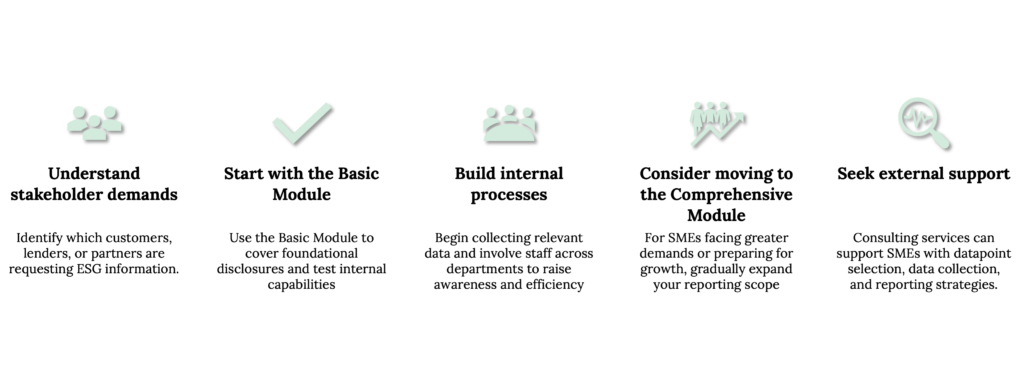

A path forward for SMEs

- Understand stakeholder demands: Identify which customers, lenders, or partners are requesting ESG information.

- Start with the Basic Module: Use the Basic Module to cover foundational disclosures and test internal capabilities.

- Build internal processes: Begin collecting relevant data and involve staff across departments to raise awareness and efficiency.

- Consider moving to the Comprehensive Module: For SMEs facing greater demands or preparing for growth, gradually expand your reporting scope.

- Seek external support: Consulting services can support SMEs with datapoint selection, data collection, and reporting strategies.

Conclusion

With its two-module approach, VSME Sustainability Reporting Standard offers flexibility and proportionality, making sustainability reporting more accessible and less resource-intensive.

Magnolia Consulting is ready to support SMEs at every step of their sustainability journey—from first-time reporters using the Basic Module to advanced SMEs preparing comprehensive disclosures. Reach out to our team to explore how your business can benefit from early adoption of the VSME Standard and align with the future of sustainable business.