The European Financial Reporting Advisory Group (EFRAG) is mandated by the European Commission to develop the sustainability reporting standards and started publishing the “European Sustainability Reporting Standards” (ESRS) in January 2022. The group published drafts for the sector-agnostic cross-cutting and topical standards for consultation in April 2022. The first set of standards, the cross-cutting and topical standards, are planned to be handed over to the EU Commission in Q4 2022 and are supposed to be adopted by the Commission by June 2023. These standards are going to be supplemented by sector-specific standards which are partly under development now and are being discussed and evaluated with relevant stakeholders since June 2022. The EFRAG plans to publish them in sector groups over the next three years, with the first ten sectors to be released in November 2023. The standards once finalised, will be mandatory for all companies that fall under the scope of the Corporate Sustainability Reporting Directive (CSRD). [1]

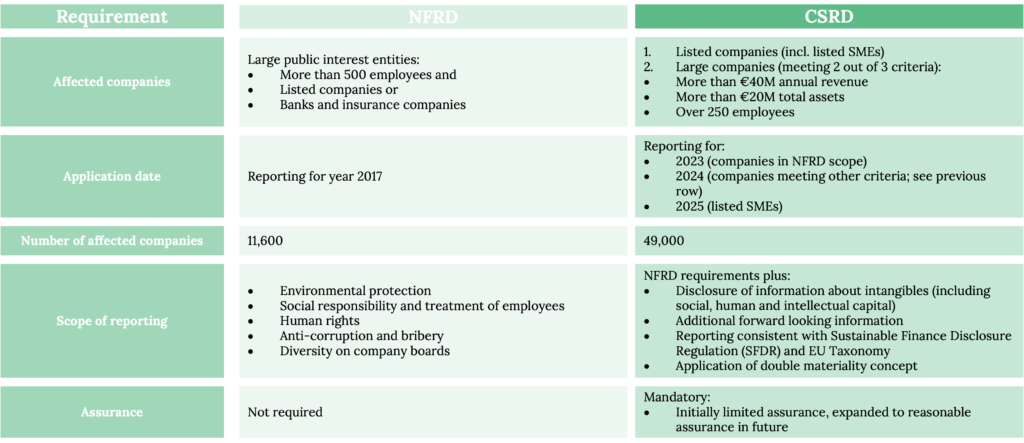

The scope will be extended to include large companies and all listed companies (incl. listed SMEs) except listed micro-companies. The scope would include companies not established in the EU that are listed on EU regulated markets, and the EU subsidiaries of Non-EU companies. In Germany companies are defined to be large (section 267 subsection 3 HGB) if they fulfil at least two of the three following criteria:

- More than €40M annual revenue

- More than €20M total assets

- Over 250 employees (on average)

Furthermore, political agreement was reached as to when the CSRD shall apply. The EU Commission initially suggested 2024 to be the first reporting year under CSRD for all large companies. The Parliament, the council and the Commission agreed to the following in the Trialogue:

- Companies that are already required to report according to the current Non-Financial Reporting Directive (NFRD) need to report according to the CSRD for the business year 2024 onwards.

- Large companies (not subject to NFRD) need to report according to CSRD for the business year 2025 onwards.

- Listed SMEs need to adhere to the CSRD for the business year 2026. [2]

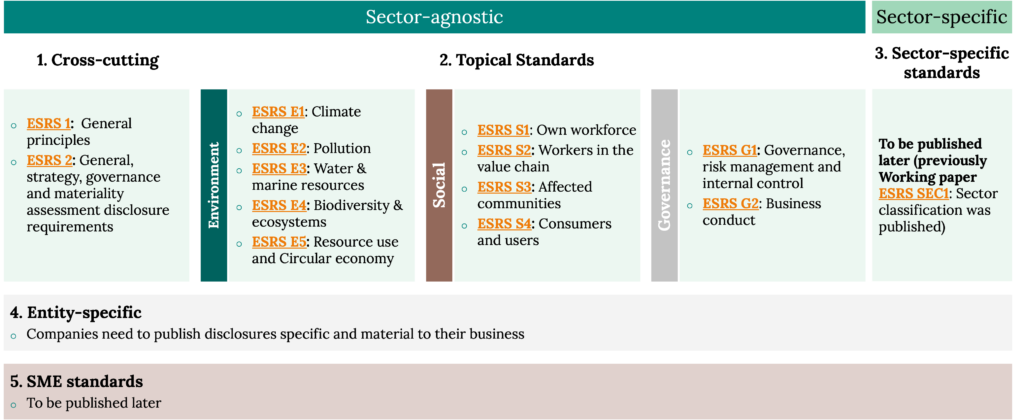

Looking at the below picture it can be stated that sustainability reporting has finally moved into a new era. While the final set of standards is still work in progress, the structure is set. Companies will need to confront themselves with sector-agnostic standards dealing with “strategy, governance, impacts, risks & opportunities” (cross-cutting standards), with topic standards around the topics environment, social and governance. For the sector-specific standards most sectors have been addressed with a first round of workshops to gain input for the preparation of draft ESRS. Some high-emitting sectors (e.g. Motor Vehicles, Energy and Utilities, Oil and Gas Mid to Downstream & Oil and Gas Upstream) are currently in the process of a second round of workshops with community sector groups to support the draft development. The companies also have to deal with conceptual guidelines around general topics such as the double materiality and with standards linked to the presentation of the information. While according to the NFRD-interpretation of many an aspect is material if both the impact and the financial materiality are relevant, the CSRD requires companies to report on sustainability aspects already if they are material according to at least one materiality perspective (impact or financial materiality). Furthermore, they will still need to analyse their business for entity-specific and material sustainability topics.

We can see that companies will have to report numerous mandatory disclosures – looking at the dramatic changes that have been published in a short period of time and looking at the current state of sustainability reporting we are convinced that it is fair to assume companies are not yet ready to report according to this new regime.

Therefore, we believe it to be crucial that companies start familiarising themselves with the standards even though they are still in a draft or working paper status. The direction for the different topics can already be seen and relevant processes can be kicked off. We recommend the following actions:

- Net Zero Targets: Already and even if not yet mandatory, we believe that companies should be analysing how they are contributing to reaching the EU's Net Zero targets, whether they have the ambitious strategies necessary in place, how their transition plans are structured and start reporting around that.

- KPIs: Companies should be looking at the KPIs that are likely to be required. If they have not computed and analysed these already, they should start collecting the necessary information.

- Extended materiality analysis: They can also already update (if not already done) their materiality analysis with respect to the double materiality. This change will probably stay for good.

While the current call for experts on specific sectors is closed the EFRAG will hold public sessions, where the participants receive a summary of the sector-specific discussion and are able to discuss the topics with all interested stakeholders.

The schedule and registration form for available events can be found here.

[1] Except the SMEs that will have to publish CSRD-reporting in the future. A set of less extensive standards will be developed for those companies.

[2] They do have the possibility to “opt-out” until the business year 2028.